Introduction: Why Budgeting is More Important Than Ever in 2025

Inflation, fluctuating interest rates, and rising living costs are making 2025 one of the trickiest years for personal finance in recent memory. Whether you’re a student just starting your career or a professional looking to optimize your savings, having a simple yet effective budgeting framework is essential.

One of the most popular and easy-to-follow systems is the 50/30/20 Rule. Made famous by U.S. Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan, this rule helps you allocate your income into needs, wants, and savings in a balanced way.

In this guide, we’ll cover:

- What the 50/30/20 Rule is and why it works in 2025

- How to apply it in India and globally

- Real-life examples and case studies

- Common mistakes and how to avoid them

- How technology and AI tools can help you stick to it

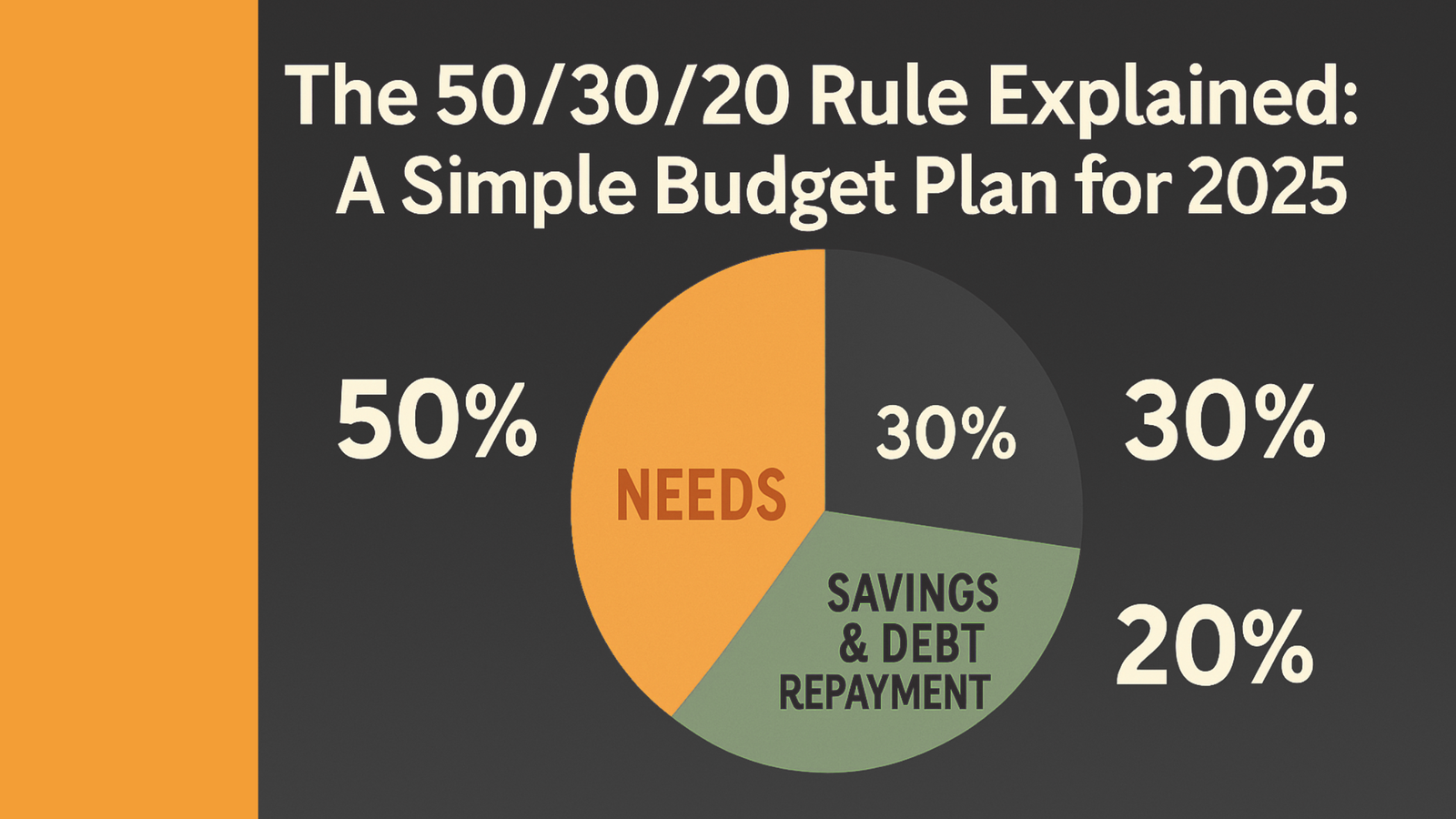

What is the 50/30/20 Rule?

The 50/30/20 Rule is a simple budgeting method that divides your after-tax income into three categories:

- 50% for Needs – Essential expenses you can’t live without

- 30% for Wants – Lifestyle and leisure expenses

- 20% for Savings & Debt Repayment – Building your future wealth

Here’s the breakdown:

| Category | Percentage of Income | Examples |

|---|---|---|

| Needs | 50% | Rent, groceries, utilities, insurance, loan EMIs |

| Wants | 30% | Dining out, streaming services, shopping, travel |

| Savings & Debt | 20% | Mutual funds, retirement accounts, emergency fund, debt repayment |

Why the 50/30/20 Rule Works in 2025

In 2025, financial discipline isn’t just about saving—it’s about balancing today’s needs with tomorrow’s goals.

- Simplicity – No complicated formulas; just three categories.

- Flexibility – Works whether you earn ₹30,000 or ₹3 lakh per month.

- Goal-Oriented – Ensures you save consistently while enjoying life.

How to Apply the 50/30/20 Rule (Step-by-Step)

Step 1: Calculate Your After-Tax Income

This is your net income after taxes, EPF contributions, and other deductions.

Tip: Use this Income Tax Calculator to get an accurate number.

Step 2: Set 50% for Needs

Needs are non-negotiable expenses that keep your life running.

Examples:

- Rent or home loan EMI

- Basic groceries and utilities

- Health insurance premiums

- Minimum loan repayments

Step 3: Allocate 30% to Wants

Wants to improve your lifestyle, but aren’t essential for survival.

Examples:

- Streaming subscriptions

- Eating out or ordering in

- Travel and weekend getaways

- Shopping for luxury goods

Step 4: Invest & Save 20%

This portion helps you build long-term wealth and financial security.

Examples:

- Mutual Funds

- Fixed Deposits (FDs)

- Retirement plans like NPS

- Emergency fund in a high-yield savings account

Example: Applying the Rule in India

Let’s assume after-tax income = ₹60,000/month.

- Needs (50%) → ₹30,000 (Rent ₹15k, Groceries ₹8k, Utilities ₹3k, Insurance ₹4k)

- Wants (30%) → ₹18,000 (Dining ₹5k, Travel ₹8k, Shopping ₹5k)

- Savings (20%) → ₹12,000 (Mutual Funds ₹7k, FD ₹2k, Emergency Fund ₹3k)

Case Study: How Priya Achieved Financial Stability in 1 Year

Priya, a 28-year-old marketing professional in Mumbai, was constantly running out of money before payday. By adopting the 50/30/20 rule, she:

- Cleared her credit card debt in 8 months

- Built an emergency fund worth 3 months of expenses

- Started investing in index funds regularly

Her stress levels dropped, and she reported feeling “in control” for the first time.

Common Mistakes to Avoid

- Not Tracking Expenses – Use apps like Walnut or Money Manager to keep track.

- Confusing Needs with Wants – A luxury coffee daily isn’t a “need.”

- Ignoring Inflation – Adjust your budget every 6-12 months.

- Skipping Debt Repayment – Debt snowball or avalanche methods work well.

Adapting the Rule for Different Incomes

- Low Income: Shift to 60/20/20 (60% needs) until income grows.

- High Income: Try 40/30/30 to speed up wealth building.

50/30/20 Rule in the Age of AI Finance Tools

Apps like YNAB (You Need a Budget) and Mint use AI to analyze your spending patterns and recommend adjustments.

Even SEBI’s new guidelines are pushing for more transparent and responsible financial advice, making it easier for beginners to make smarter choices.

External Resources to Explore

- Investopedia’s Guide to Budgeting

- Reserve Bank of India – Financial Education

- National Pension System (NPS) Information

Conclusion: The Rule That Works if You Do

The 50/30/20 Rule is not magic—it’s discipline disguised as simplicity. Whether you earn in rupees or dollars, this budgeting system keeps your spending, saving, and lifestyle in harmony.

In 2025’s uncertain economy, the people who will thrive are not necessarily the highest earners, but the ones who spend with intention and save with purpose.

Disclaimer

This article is for educational purposes only and does not constitute financial advice. Please consult a certified financial planner or investment advisor before making any financial decisions.